Healthcare Logistics Market Size, Share

Report Overview

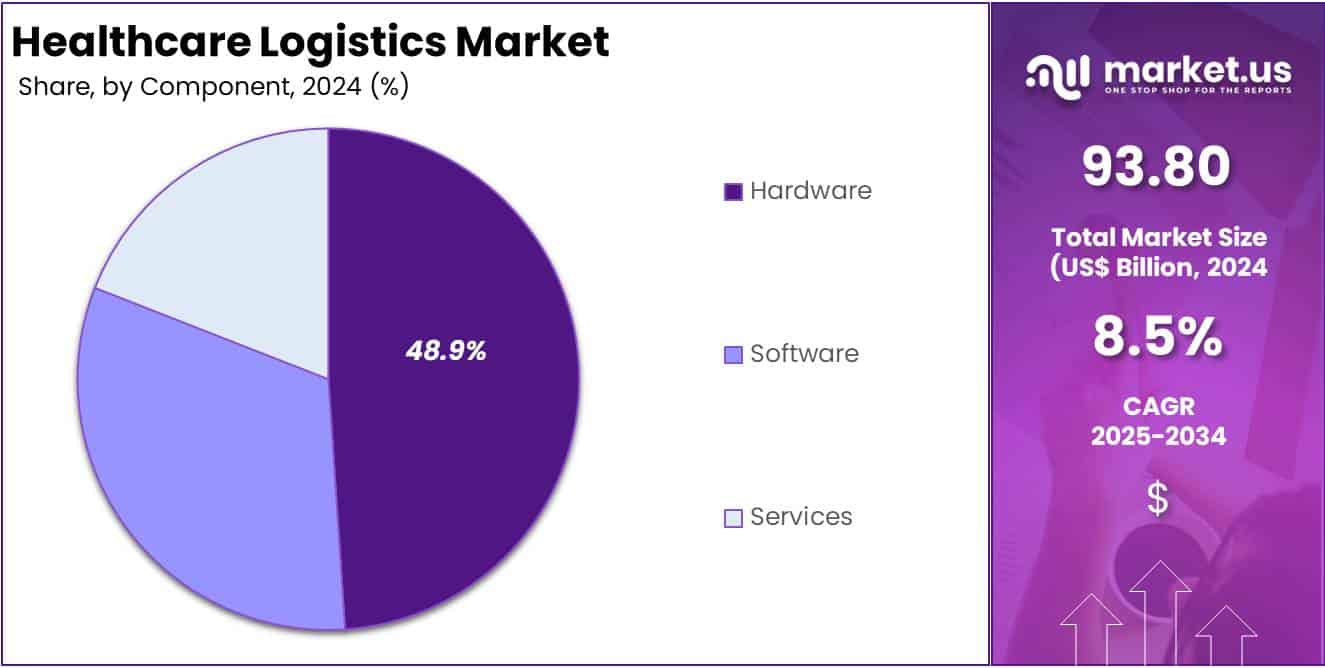

The Global Healthcare Logistics Market size is expected to be worth around US$ 217.3 Billion by 2034, from US$ 93.8 Billion in 2024, growing at a CAGR of 8.5% during the forecast period from 2025 to 2034.

The Global Healthcare Logistics Market is essential for the transportation, storage, and delivery of medical goods such as pharmaceuticals, medical devices, and equipment, experiencing significant growth due to increasing healthcare demands, especially in emerging markets, the rise of e-commerce, and the need for cold chain logistics.

- By 2050, 16% of the global population is projected to be over 65, with Europe and North America reaching 27%. This demographic shift is increasing the demand for healthcare services, particularly for age-related conditions.

- The prevalence of diabetes among adults has surged more than fourfold since 1990, now exceeding 800 million globally. This rise is closely linked to increased obesity, unhealthy diets, physical inactivity, and economic hardship.

- Approximately 55% of the global population lacks access to essential health services. In low-income countries, only 1 in 5 people have access to basic healthcare, highlighting significant disparities in healthcare access.

The market is segmented into various categories, including transportation, warehousing, and cold chain logistics. Transportation is critical in ensuring the timely delivery of medicines, surgical supplies, and other essential items, especially with the growing reliance on e-commerce and global supply chains. Cold chain logistics plays a pivotal role in maintaining the integrity of temperature-sensitive pharmaceuticals, such as vaccines, biologics, and blood products. With the COVID-19 pandemic, the importance of cold chain logistics has been amplified due to the distribution of vaccines and other temperature-controlled medical products.

The market is also influenced by regulatory requirements and technological advancements. Strict regulations surrounding the transportation of pharmaceuticals and medical devices ensure safety, compliance, and the prevention of contamination. Innovations in tracking technologies, real-time monitoring systems, and automated warehouses are improving efficiency, reducing costs, and enhancing transparency in the supply chain.

North America holds a significant share of the global healthcare logistics market, owing to the region’s well-established healthcare infrastructure and technological advancements. However, Asia-Pacific is expected to witness the highest growth, driven by the expanding healthcare sector, increasing investment in logistics infrastructure, and a rising demand for quality healthcare services.

In conclusion, the global healthcare logistics market is poised for continued growth, supported by technological innovations, an aging population, and increasing healthcare needs, along with the rising demand for global distribution and efficient logistics solutions in the sector.

Key Takeaways

- The Healthcare Logistics market generated a revenue of US$ 93.80 Million and is predicted to reach US$ 217.33 Million, with a CAGR of 8.5%.

- Based on the Product, the Pharmaceutical products segment generated the most revenue for the market with a market share of 68.10%.

- Based on the Component, the Hardware segment generated the most revenue for the market with a market share of 48.9%.

- Based on the mode, the Outsourcing segment generated the most revenue for the market with a market share of 58.9%.

- Based on the logistics type, the outbound logistics segment generated the most revenue for the market with a market share of 47.8%.

- Based on the Supply Chain, the Cold-chain supply chain logistics segment generated the most revenue for the market with a market share of 53.6%.

- Based on the end-user, the Pharmaceutical and biotechnology companies segment generated the most revenue for the market with a market share of 36.1%.

- Region-wise, North America remained the lead contributor to the market, by claiming the highest market share, amounting to 31.60%.

Product Analysis

Based on product the market is categorized by Pharmaceutical products and Medical devices and equipment. The pharmaceutical products segment dominates the global healthcare logistics market, holding a significant 68.10% market share. This dominance is driven by the increasing demand for pharmaceuticals, including drugs, vaccines, and biologics, which require specialized logistics solutions such as cold-chain transportation and real-time monitoring.

The growing prevalence of chronic diseases, rising vaccination programs, and expanding biopharmaceutical innovations contribute to the segment’s growth. The COVID-19 pandemic further highlighted the need for efficient pharmaceutical logistics, accelerating investments in temperature-controlled supply chains and digital tracking solutions.

Additionally, government regulations mandating Good Distribution Practices (GDP) for pharmaceuticals have strengthened the infrastructure for healthcare logistics. Emerging markets in Asia-Pacific and Latin America are witnessing rapid growth due to expanding pharmaceutical production and distribution networks. With continuous advancements in logistics technology, including AI-driven route optimization and blockchain-based tracking, the pharmaceutical segment is expected to maintain its dominant position in the healthcare logistics market.

- Over 9,000 medicines are currently under development globally, with 1,488 drugs targeting infectious diseases, 3,148 for cancer, 451 for diabetes, and 1,668 for neurologic disorders, spanning Phase I to Phase III of development.

Component Analysis

The hardware segment dominated the global healthcare logistics market, driven by the increasing demand for automated storage and retrieval systems (AS/RS), RFID tracking, IoT-enabled sensors, and temperature-controlled logistics equipment. These technologies ensure the safe handling and transportation of pharmaceuticals and medical devices, particularly for cold-chain logistics.

With the rise of biopharmaceuticals and precision medicine, real-time monitoring and secure storage solutions have become essential. The integration of AI and automation in warehouses and distribution centers further boosts efficiency. As healthcare logistics continue to evolve, investments in hardware infrastructure will remain crucial for ensuring supply chain reliability and compliance.

Mode Analysis

Outsourcing and In-house are the two modes in the global healthcare logistics market. The outsourcing segment accounted for 58.9% of the global healthcare logistics market in 2024, driven by the increasing reliance on third-party logistics (3PL) providers for cost efficiency and expertise. Pharmaceutical and medical device companies outsource logistics to specialized providers that offer temperature-controlled transportation, inventory management, and regulatory compliance solutions.

The growth of biopharmaceuticals, personalized medicine, and global vaccine distribution has heightened demand for secure and efficient logistics services. Outsourcing also allows companies to focus on core competencies while leveraging advanced AI-driven tracking, blockchain security, and real-time monitoring offered by logistics partners, ensuring a robust supply chain.

Logistics Type Analysis

The outbound logistics segment held the largest market share in the global healthcare logistics market in 2024, driven by the growing demand for efficient distribution of pharmaceuticals, medical devices, and biologics. This segment includes the transportation of healthcare products from manufacturers to hospitals, pharmacies, and end-users, requiring temperature-sensitive logistics and real-time tracking.

With the rise of e-commerce in healthcare, direct-to-patient delivery models and automated distribution centers have further boosted outbound logistics. Regulatory compliance, cold-chain solutions, and AI-powered route optimization are key factors enhancing efficiency. As demand for timely and secure medical deliveries rises, outbound logistics will continue to dominate.

Supply Chain Analysis

The cold-chain supply chain dominated the global healthcare logistics market in 2024, driven by the increasing demand for temperature-sensitive pharmaceuticals, vaccines, biologics, and specialty drugs. This segment plays a crucial role in ensuring the integrity, efficacy, and safety of healthcare products that require strict temperature control during storage and transportation. The rise of biopharmaceuticals and gene therapies, along with global vaccination programs, has significantly boosted the need for advanced cold-chain logistics solutions.

Companies are investing in IoT-enabled temperature monitoring, real-time tracking, and AI-powered predictive analytics to enhance supply chain efficiency. Stringent regulatory requirements, such as Good Distribution Practices (GDP), have further strengthened cold-chain logistics infrastructure. With emerging markets expanding healthcare access, the demand for specialized refrigeration, insulated packaging, and cold storage facilities will continue to drive this segment’s dominance in the healthcare logistics industry.

Key Market Segments

By Products

- Pharmaceutical products

- Drugs

- Vaccines

- Other pharmaceutical products

- Medical devices and equipment

By Component

- Hardware

- Software

- Services

By Mode

By Logistics Type

- Inbound logistics

- Outbound logistics

- Reverse logistics

By Supply Chain

- Cold-chain supply chain

- Non cold-chain supply chain

By End-use

- Pharmaceutical and biotechnology companies

- Healthcare facilities

- Medical device companies

- Other end-users

Drivers

Rising Demand for Pharmaceuticals & Biopharmaceuticals

The rising demand for pharmaceuticals and biopharmaceuticals is a major driver of the global healthcare logistics market, necessitating advanced and specialized supply chain solutions. With the increasing production and distribution of vaccines, biologics, and personalized medicines, there is a growing need for temperature-controlled logistics, secure transportation, and real-time monitoring to maintain product integrity.

Biopharmaceuticals, including gene therapies, monoclonal antibodies, and cell-based treatments, require cold-chain solutions to preserve efficacy. The expansion of global vaccination programs and the growing prevalence of chronic diseases have further heightened demand for reliable pharmaceutical logistics.

Additionally, personalized medicine involves tailored treatments with shorter shelf lives, requiring rapid and efficient delivery networks. Companies are investing in IoT, blockchain, and AI-powered tracking systems to enhance supply chain transparency. Regulatory requirements, such as Good Distribution Practices (GDP), further emphasize the need for high-quality storage and transportation, ensuring patient safety and treatment effectiveness.

Restrains

Limited Cold-Chain Infrastructure in Emerging Markets

The limited cold-chain infrastructure in emerging markets remains a significant challenge in the global healthcare logistics market, affecting the safe distribution of temperature-sensitive pharmaceuticals, vaccines, and biologics. Many developing regions, particularly in Africa, Southeast Asia, and Latin America, lack refrigerated storage facilities, specialized transportation, and trained personnel to manage cold-chain logistics effectively. The demand for biopharmaceuticals, gene therapies, and vaccines has surged, but inadequate infrastructure leads to spoilage, reduced efficacy, and financial losses.

Insufficient investment in cold storage warehouses, insulated transport vehicles, and real-time monitoring systems further exacerbates the issue. Additionally, power supply instability, regulatory challenges, and poor last-mile connectivity hinder the reliability of healthcare supply chains in these regions. To address this, governments and private sectors are investing in cold-chain expansions, technology integration (IoT and blockchain), and workforce training programs. Strengthening cold-chain capabilities is crucial to ensuring equitable access to life-saving medications and vaccines worldwide.

Opportunities

Growth in E-Commerce and Direct-to-Patient Deliveries

The growth in e-commerce and direct-to-patient deliveries is reshaping the global healthcare logistics market, with the rise of online pharmacies and telemedicine playing a key role. As patients increasingly opt for online pharmaceutical services and virtual healthcare consultations, the demand for efficient and secure last-mile delivery solutions has surged.

E-commerce platforms are driving the need for automated warehousing, real-time inventory management, and smart order fulfillment systems to ensure fast and accurate deliveries of medications, medical devices, and healthcare products. These platforms also require specialized logistics for temperature-sensitive items like vaccines and biologics.

Telemedicine growth has increased the demand for direct-to-patient shipments, particularly for chronic disease management, prescription refills, and specialty medicines. To meet these needs, healthcare logistics providers are investing in automated sorting systems, last-mile delivery optimization, and flexible transportation networks. This trend is also improving patient convenience, medication adherence, and overall healthcare accessibility.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the global healthcare logistics market, influencing cost structures, supply chain efficiency, and access to medical products.

Economic downturns or recessions can strain budgets for healthcare logistics, limiting investments in infrastructure and technology. Rising fuel prices and inflation increase the cost of transportation and storage, making logistics more expensive and reducing profit margins for service providers.

Geopolitical instability, such as trade wars, sanctions, or conflicts, disrupts global supply chains and delays the transportation of critical healthcare products. This is particularly problematic for cold-chain logistics, where delays can compromise product efficacy.

Furthermore, political unrest in emerging markets can hinder the development of healthcare infrastructure, affecting the distribution of essential medical supplies. Regulatory changes, such as stricter import/export laws or changing compliance standards, also create challenges for logistics providers operating internationally. These factors demand adaptive strategies and resilient supply chains to mitigate risks.

Latest Trends

The global healthcare logistics market is witnessing several emerging trends driven by technological advancements and evolving consumer expectations. The integration of AI, IoT, blockchain, and robotics is enhancing supply chain efficiency through real-time tracking, route optimization, and predictive analytics, while blockchain ensures better transparency and security, especially for pharmaceutical traceability. The growing demand for biopharmaceuticals, vaccines, and personalized medicines has spurred the expansion of cold-chain logistics.

Additionally, innovations in last-mile delivery and e-commerce are pushing for automated sorting and the use of drones and robotics to meet fast delivery expectations. Sustainability is also a key focus, with logistics providers adopting eco-friendly packaging, carbon-neutral transportation, and energy-efficient warehouses to align with environmental goals and regulatory requirements.

Regional Analysis

North America Dominates the Global Healthcare Logistics Market

North America holds a leading position in the global healthcare logistics market, primarily due to its well-established healthcare infrastructure and the extensive use of advanced technology. The region experiences a high demand for pharmaceuticals, medical devices, and biopharmaceuticals. These factors collectively enhance the efficiency of healthcare services and product availability across North America.

The region benefits significantly from its robust cold-chain logistics infrastructure, which is crucial for the distribution of temperature-sensitive healthcare products. This infrastructure is particularly vital for the handling and transportation of vaccines, biologics, and specialty drugs, ensuring they remain effective throughout their delivery process.

The United States, in particular, has seen significant growth in biopharmaceutical production and personalized medicine, which require advanced supply chain solutions, including AI, IoT, and blockchain technologies for real-time tracking and compliance. E-commerce growth and direct-to-patient deliveries further fuel demand for last-mile delivery solutions and automated warehousing.

Additionally, stringent regulatory frameworks, such as FDA guidelines and Good Distribution Practices (GDP), ensure the safety and efficacy of medical shipments, enhancing market growth. The presence of leading logistics companies and continuous investments in innovation contribute to North America’s dominance, positioning it as a leader in healthcare logistics globally.

Key Regions and Countries

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the Global Healthcare Logistics Market, several key players dominate the market share, leveraging advanced technologies and extensive distribution networks. DHL Supply Chain, Kuehne + Nagel, and UPS Healthcare are among the leaders, with substantial shares due to their global reach, comprehensive cold-chain solutions, and robust logistics infrastructure. These companies focus on temperature-controlled transportation, real-time monitoring, and regulatory compliance, catering to the growing demand for biopharmaceuticals and personalized medicines.

XPO Logistics and C.H. Robinson are also prominent, offering specialized healthcare logistics services, including last-mile delivery, automated warehousing, and AI-driven supply chain management. Smaller, niche players are gaining market share by focusing on specific needs such as direct-to-patient deliveries or innovative packaging solutions.

The competition in the market is intensified by continuous investments in technology, automation, and sustainability. Companies are also expanding their presence in emerging markets, addressing the increasing demand for healthcare products and services globally.

Top Key Players in the Healthcare Logistics Market

- Agility

- H. Robinson

- Cardinal Health

- CERNER

- CEVA Logistics

- DB Group

- DSV

- FedEx

- Infor

- Kerry Logistics

- Kuehne + Nagel

- Nippon Express

- Oracle

- SAP SE

- SF Express

Recent Developments

- In June 2024, a strategic partnership between MG Real Estate, GSK, and Yusen Logistics was announced to establish the largest biopharmaceutical warehouse in Belgium. The facility will feature cutting-edge automated robotics and advanced software to optimize operations. This collaboration underscores the growing reliance on automation and technological innovation to scale biopharmaceutical logistics efficiently.

- In February 2023, DHL announced a USD 200 million investment in the U.S. to strengthen its pharmaceutical and life sciences supply chain capabilities. The company plans to build a state-of-the-art warehouse focused on healthcare products, further solidifying its position as a leader in the healthcare logistics industry.

Report Scope

link