U.S. Medical Equipment Market Size & Share, 2033

U.S. Medical Equipment Market Size

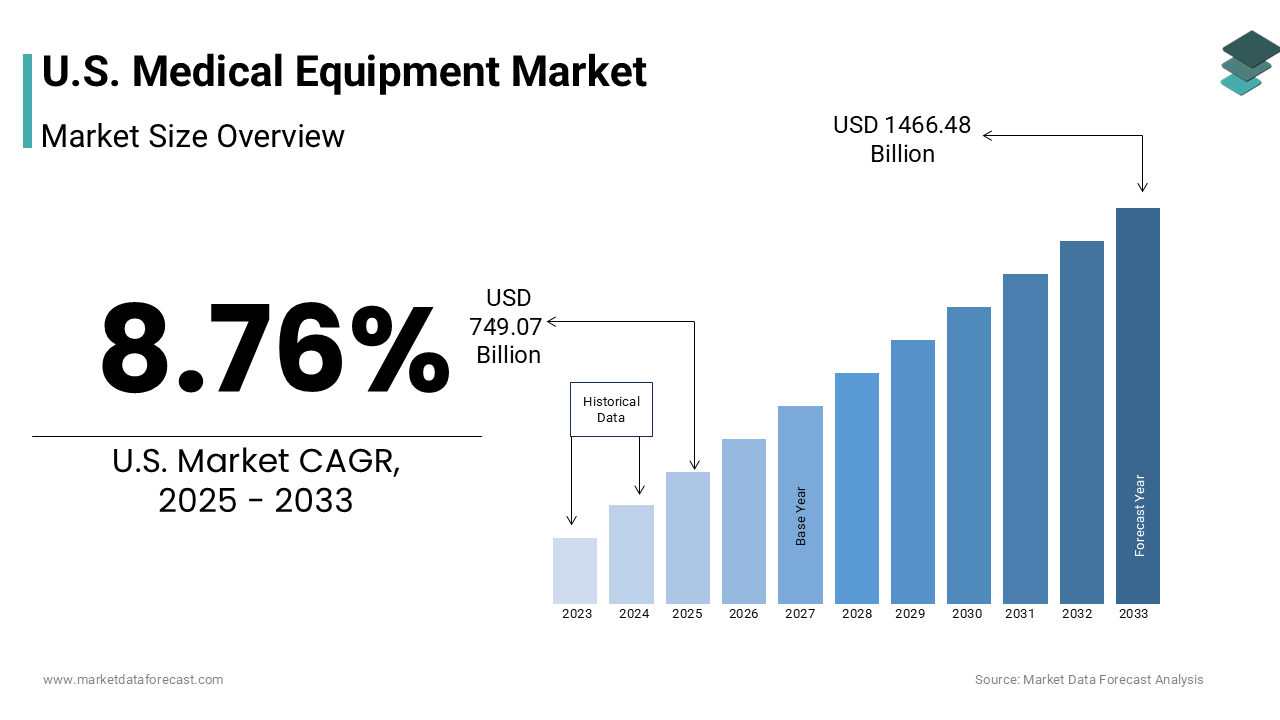

The U.S. medical equipment market size was valued at USD 688.74 billion in 2024 and is anticipated to reach USD 749.07 billion in 2025 from USD 1466.48 billion by 2033, growing at a CAGR of 8.76% during the forecast period from 2025 to 2033.

Medical equipment is diagnostic, therapeutic, and monitoring devices engineered to support clinical decision-making, surgical intervention, and chronic disease management within institutional and home-based care environments. As per the Centers for Disease Control and Prevention, over 36 million inpatient surgeries are performed annually in the United States, each requiring a suite of sterile, precision-engineered instruments, from electrosurgical units to image-guided navigation systems. Escalating procedural volume, workforce shortages, and value-based reimbursement are collectively reshaping equipment design toward interoperability, predictive maintenance, and AI-augmented usability.

MARKET DRIVERS

The inexorable rise in surgical volume surges the growth rate of the U.S. medical equipment market. It is driven by an aging population and expanding indications for minimally invasive interventions. As per the American College of Surgeons, the number of individuals aged 65 and older undergoing elective surgery has increased, a cohort projected to reach 80 million by 2040, according to the U.S. Census Bureau. This demographic inevitability fuels adoption of robotic platforms. Intuitive Surgical’s da Vinci system supports over 1.5 million annual procedures, with robotic-assisted prostatectomies have been associated with fewer complications compared to open technique. Simultaneously, CMS’s New Technology Add-On Payment program reimburses by incentivizing capital investment despite upfront costs per unit.

The federal mandate for hospital interoperability and real-time device-to-EHR data integration also contributes to the expansion of the U.S. medical equipment market. As per sources, a portion of acute care hospitals must now transmit structured device data, including ventilator settings, infusion pump logs, and telemetry vitals, directly into certified EHRs without manual re-entry. This regulatory compulsion has triggered mass adoption of smart infusion pumps with dose-error reduction systems, which the ECRI Institute credits with preventing a portion of medication administration errors in ICUs. Some companies have embedded HL7 FHIR APIs into a portion of new monitor shipments since 2023, while the FDA now requires cybersecurity risk assessments for all network-connected devices, a stipulation accelerating lifecycle management software adoption.

MARKET RESTRAINTS

Protracted capital budgeting cycles and stringent health technology assessment protocols that delay equipment procurement by several months in public and nonprofit institutions, and this restrains the growth of the U.S. medical equipment market. According to sources, hospitals in the United States are facing delays in equipment purchasing approvals due to lengthy evaluation and financial review processes. As per studies, most advanced medical technologies require multiple validation trials before receiving final funding. As per research, financial regulations and depreciation schedules often discourage investment in high-cost clinical devices despite their proven utility.

The acute shortage of biomedical equipment technicians capable of maintaining, calibrating, and securing increasingly software-dependent devices further slows down the expansion of the U.S. medical equipment market. The current biomedical technician workforce is struggling to keep pace with rising demand across hospitals and surgical centers, according to sources. Many healthcare facilities are operating with limited staff, which often leads to longer equipment downtime and higher maintenance costs, as per studies. Frequent cybersecurity updates for connected medical devices are becoming harder to manage internally, which increases dependence on external service providers, as per research.

MARKET OPPORTUNITIES

The retrofitting of legacy equipment with AI-powered predictive maintenance modules to extend service life and avoid capital replacement opens new opportunities for the growth of the U.S. medical equipment market. As per research, advanced machine learning systems can predict certain medical equipment failures well before they occur. Furthermore, according to sources, funding initiatives are supporting the development of diagnostic tools designed to reduce unexpected downtime in hospital settings. Public healthcare agencies are implementing predictive maintenance programs that private hospitals are beginning to adopt.

The decentralization of acute-care-grade monitoring into home settings via FDA-cleared and cellular-enabled devices reimbursed under CMS’s Remote Therapeutic Monitoring codes, which generates potential opportunities for the U.S. medical equipment market. More patients are eligible for remote patient monitoring reimbursement, according to sources. In addition, home-based hemodynamic tracking is gaining recognition as an effective approach for managing certain heart conditions, as per studies. Insurance coverage for connected infusion pumps in home chemotherapy is helping reduce hospital stays while ensuring treatment safety.

MARKET CHALLENGES

The lack of standardized cybersecurity frameworks for legacy medical devices challenges the growth of the U.S. medical equipment market. This leaves a portion of installed equipment vulnerable to ransomware and data exfiltration. Also, many hospitals continue to operate medical devices that rely on outdated software systems, according to sources. Regulatory updates now require stronger cybersecurity measures for new equipment but often exclude older models still in use, as per studies. Unpatched devices have contributed to several major network breaches across healthcare systems, which emphasizes the need for greater collaboration with manufacturers to manage risks.

The misalignment between device usability design and real-world clinical workflows also constrains the expansion of the U.S. medical equipment market. And, this leads to alarm fatigue, configuration errors, and underutilization of advanced features. Many intensive care staff override default safety settings on medical devices to reduce workflow interruptions, according to sources. Surgical teams often turn off alerts they consider unnecessary, which can increase the risk of near-miss incidents, as per studies. As per research, only a handful of hospitals perform usability testing after installation, despite extensive usability validation being recommended by human factors guidelines. As a result, several advanced systems remain underused in smaller hospitals, not because of faults, but due to differences in staffing and operational setups

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Type, Product, End user, and Region. |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

|

Key Market Players |

Medtronic (USA), Johnson & Johnson, Abbott Laboratories, GE Healthcare, Siemens Healthineers, Boston Scientific, Stryker Corporation, Becton, Dickinson and Company (BD), Baxter International, Zimmer Biomet Holdings, 3M Company, B. Braun, Medline Industries, Intuitive Surgical, and Edwards Lifesciences. |

SEGMENTAL ANALYSIS

By Type Insights

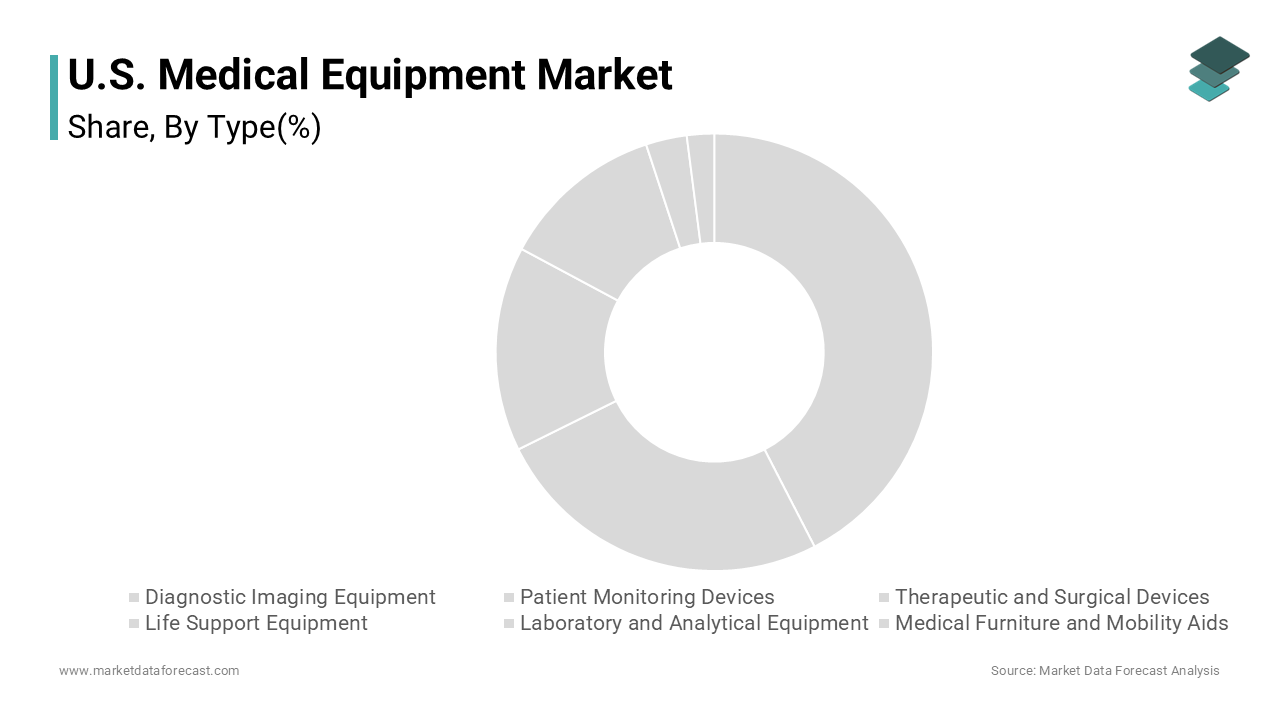

The diagnostic imaging equipment segment held the leading share of 22.5% of the U.S. medial equipment market in 2024. The dominance of the diagnostic imaging equipment segment due to care infrastructure. Advanced imaging is an essential component in most cancer treatment plans and trauma cases, according to sources. Insurance reimbursement supports the large-scale use of these procedures across healthcare systems, as per studies. AI-enabled imaging platforms are being adopted more quickly through regulatory fast-track programs, improving clinician efficiency, as per research.

The patient monitoring devices segment is predicted to witness the highest CAGR of 13.9% from 2025 to 2033. The growth of the patient monitoring devices segment is propelled by CMS’s expansion of Remote Patient Monitoring reimbursement codes and hospital adoption of predictive analytics. Certain advanced monitoring platforms have been shown to improve outcomes for critically ill patients, according to sources. Large healthcare networks are increasingly using wearable biosensors to identify serious conditions earlier, as per studies. Safety guidelines require continuous monitoring for specific post-operative patients, which boosts demand for devices with advanced respiratory tracking features.

By Product Insights

The disposables and consumables segment remained the prominent segment and captured 58.5% share in 2024. The dominance of the disposables and consumables segment is attributed to the procedural volume and infection control mandates. According to sources, sterilization guidelines in healthcare mandate the use of single-use devices for various surgical and clinical applications. As per studies, common surgical procedures often require a significant number of disposable items that add to overall procedural costs. Besides, as per research, financial penalty programs are motivating hospitals to adopt infection-prevention products that help improve patient safety outcomes.

The instruments and equipment segment is estimated to register the fastest CAGR of 9.6% during the forecast period due to AI integration, robotic automation, and value-based reimbursement. According to sources, new robotic systems for lung diagnosis are being rapidly adopted in hospitals after receiving regulatory approval. As per studies, financial reimbursement policies are helping healthcare providers manage the high costs of advanced robotic procedures by encouraging broader integration of such technologies. As per research, hospitals are also focusing on predictive maintenance tools that use artificial intelligence to reduce equipment downtime and improve efficiency. These innovations are not only improving clinical accuracy and turnaround times but are also transforming expensive medical equipment into smarter and data-driven assets that deliver long-term operational value.

By End User Insights

The hospitals and clinics segment led the U.S. medical equipment market by occupying substantial market in 2024. Factors such as regulatory mandates, procedural complexity, and capital infrastructure are fuelling the expansion of the hospitals and clinics segment. According to sources, intensive care units are required to maintain close nurse supervision and advanced monitoring systems for every patient, which increases the need for high-value medical equipment. As per studies, top-tier trauma centers must operate with comprehensive diagnostic infrastructure by ensuring immediate access to essential imaging and laboratory tools. As per research, reimbursement models linked to patient acuity are motivating hospitals to expand their use of rapid diagnostic technologies and point-of-care testing. Together, these requirements have encouraged healthcare facilities to invest heavily in advanced equipment, integrating technology at every level of patient care to enhance efficiency, safety, and compliance with accreditation standards.

The homecare and diagnostic centers segment is anticipated to witness the fastest CAGR of 17.2% from 2025 to 2033. The rapid growth of the homecare and diagnostic centers segment is propelled by CMS’s Hospital-at-Home waiver program and private payer adoption of value-based bundles. Health insurers are expanding coverage to include connected medical devices that support patient recovery at home, according to sources. Retail health providers are introducing diagnostic tools like portable imaging systems to make chronic disease monitoring more accessible, as per studies. Home-based cardiovascular monitoring is gaining momentum through guideline updates that encourage the use of wearable devices, as per research. These combined trends are reshaping the healthcare delivery model by shifting portions of post-acute and chronic care from hospitals to patient homes, improving convenience, lowering readmission rates, and fostering continuous remote supervision under value-based care frameworks.

REGIONAL ANALYSIS

United States Medical Equipment Market Analysis

The United States is the largest medical equipment market. High procedural volume, fragmented payer dynamics, regulatory complexity, and innovation tolerance are driving the growth of the U.S. According to sources, hospitals in the United States continue to perform significantly more advanced imaging procedures than many other developed regions which reflectes a strong reliance on diagnostic technology. As per studies, regulatory initiatives are accelerating the approval of innovative medical equipment, positioning the country as a leader in adopting breakthrough devices. As per research, the healthcare reimbursement system, while complex, creates financial motivation for hospitals to implement new technologies backed by measurable outcome improvements. This dynamic reinforces a cycle of innovation where clinical performance data drives both regulatory approval and reimbursement alignment by ensuring that technological advancement remains integrated with patient care goals and institutional strategy.

Product innovation anchored in AI and workflow interoperability remains central, with firms embedding predictive analytics, EHR integration, and cybersecurity into legacy platforms. Strategic channel diversification particularly into home health and retail clinics expands access beyond hospitals. Companies aggressively pursue FDA Breakthrough Device designation and CMS New Technology Add-On Payments to justify premium pricing. Collaborative training ecosystems certify clinicians on robotic and AI platforms, ensuring adoption velocity. Lastly, regional product localization, adapting devices for power constraints, language interfaces, and disease prevalence ensures relevance in both U.S. value-based systems and Asia Pacific public health infrastructure.

COMPETITIVE LANDSCAPE

The U.S. medical equipment market is a capital-intensive, regulation-driven arena where global medtech titans compete with agile robotics and AI startups through clinical validation, reimbursement engineering, and care setting expansion. Incumbents leverage GPO contracts and hospital reference sites, while disruptors target outpatient and home-based niches with modular, software-defined devices. Regulatory arbitrage, particularly around FDA’s QSR modernization and CMS’s RPM codes, defines competitive velocity. Simultaneously, consolidation accelerates as firms acquire predictive maintenance, tele-ICU, and cybersecurity assets. Competition is no longer device-centric. It’s ecosystem-driven, demanding end-to-end solutions spanning installation, training, data integration, and lifecycle management, which turns every piece of equipment into a connected and reimbursable node in the care continuum.

KEY MARKET PLAYERS

A few of the major companies in the global U.S. medical equipment market include

- Medtronic (USA)

- Johnson & Johnson

- Abbott Laboratories

- GE Healthcare

- Siemens Healthineers

- Boston Scientific

- Stryker Corporation

- Becton, Dickinson and Company (BD)

- Baxter International

- Zimmer Biomet Holdings

- 3M Company

- B. Braun

- Medline Industries

- Intuitive Surgical

- Edwards Lifesciences

Top Strategies Used by Key Market Participants

Product innovation anchored in AI and workflow interoperability remains central, with firms embedding predictive analytics, EHR integration, and cybersecurity into legacy platforms. Strategic channel diversification particularly into home health and retail clinics expands access beyond hospitals. Companies aggressively pursue FDA Breakthrough Device designation and CMS New Technology Add-On Payments to justify premium pricing. Collaborative training ecosystems certify clinicians on robotic and AI platforms, ensuring adoption velocity. Lastly, regional product localization adapting devices for power constraints, language interfaces, and disease prevalence ensures relevance in both U.S. value-based systems and Asia Pacific public health infrastructure

MARKET SEGMENTATION

This research report on the U.S. medical equipment market has been segmented & sub-segmented into the following categories.

By Type

- Diagnostic Imaging Equipment

- Patient Monitoring Devices

- Therapeutic and Surgical Devices

- Life Support Equipment

- Laboratory and Analytical Equipment

- Medical Furniture and Mobility Aids

By Product

- Disposables and Consumables

- Instruments and Equipment

- Software and Digital Solutions

- Accessories and Spare Parts

By End User

- Hospitals and Clinics

- Homecare and Diagnostic Centers

- Ambulatory Surgical Centers (ASCs)

- Research and Academic Institutes

- Long-term Care Facilities and Nursing Homes

By Country

link